When was the last time you got paid the same day you finished a job? If you’re running a B2B or service business, almost never.

You send the invoice, add terms like Net 30 or Net 60, and then…you wait. That gap between finishing the work and actually getting paid is what’s known as accounts receivable (AR).

It’s also one of the main reasons profitable businesses still feel broke. Your sales can look strong, and your projects can be landing on time, while your bank balance tells a different story.

By the end of this guide, you’ll know exactly how AR hits your cash flow and how to forecast it so it doesn’t blindside you.

What is accounts receivable?

The accounts receivable are the amount of money owed to you by your customers who have purchased your products or services but have yet to pay.

Your balance sheet lists AR as a current asset because you expect to collect it within 30 to 90 days. You don’t have the cash yet, but your business owns that claim, and that makes it an asset.

Accrual accounting is why this works the way it does. It records revenue the moment you invoice, not when the cash arrives. So when you send an invoice, your income statement picks up the sale, and your balance sheet picks up the receivable at the same time.

In financial statements, you may also find accounts receivable being referred to as trade receivables. They mean the same thing.

At this point, you might have questions:

Is accounts receivable an asset or a liability?

Accounts receivable is not a liability but is an asset at all times. I believe this throws off many first-time founders since the money is not yet in your account, so it does not feel like it is part of your business. But it is. It represents money someone owes your business, and that makes it valuable to your business.

The only time AR gets complicated is when a customer isn’t going to pay. At that point, it doesn’t flip to a liability. Instead, it either gets reduced through an allowance for doubtful accounts or written off entirely. I’ll cover both of those in more detail later in this blog.

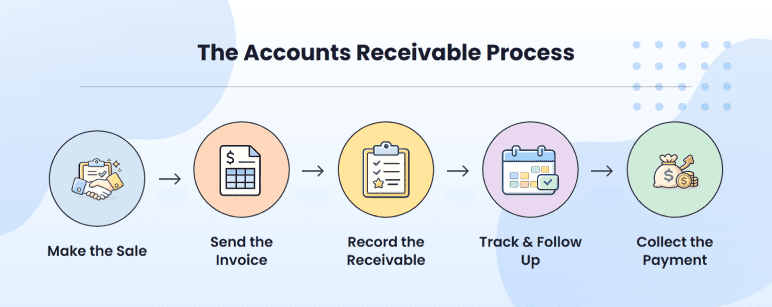

How does accounts receivable actually work?

It starts when you make a sale but don’t get paid immediately. You can have terms such as Net 30 (you must pay within 30 days of the invoice date) or Net 60 (you must pay within 60 days of the invoice date). After delivery of work, you provide an invoice with the amount, the date of payment, and the terms of payment.

You then enter the receivable in your books. The revenue is recorded immediately, although the cash has not yet been received. This usually leads to a practical question: when the sale is counted, why does cash remain tight? The answer is simple. Until the payment arrives, that revenue can’t be used to run your business.

From there, you track and follow up. This is where most businesses either stay in control or start slipping. I’d argue it’s rarely because customers refuse to pay. It’s because invoices went out late, terms weren’t clear, or nobody followed up on time. One or two delayed payments may not be a huge issue, but when you have several invoices, it begins to drag your cash cycle.

The last step is to take the cash and clear the receivable when the customer pays. The value transfers out of accounts receivable.

This entire cycle creates a gap between earning and getting paid. How you manage that gap determines whether your business feels stable or constantly short on cash.

I find the concept clicks fastest when you see it with actual numbers. Here’s a real example.

Accounts receivable example

Say you complete a project for a client and send an invoice for $5,000 on Net 30 terms. On Day 1, even though no cash has come in, you record the sale. Your books now show $5,000 in revenue and $5,000 in accounts receivable.

| Date | Account | Debit ($) | Credit ($) |

| Day 1 | Accounts Receivable | 5,000 | |

| Day 1 | Service Revenue | 5,000 | |

| Day 25 | Cash | 5,000 | |

| Day 25 | Accounts Receivable | 5,000 |

On Day 1, your business looks like it made $5,000, but nothing has changed in your bank account. You still have the same cash as before.

Now extend that across multiple clients. Say you have $20,000 in unpaid invoices at any given time. That’s $20,000 you’ve earned but can’t use. Expenses continue, but cash isn’t coming in at the same pace.

Accounts receivable is not just an accounting entry; it’s a timing problem. The longer the gap between Day 1 and Day 25, the more pressure it puts on your cash.

That example shows one side of the transaction, money that’s owed to you. But every business has the opposite side running at the same time. While you’re waiting to collect from customers, you’re also receiving bills from vendors, tools you use, and services you depend on. That’s accounts payable.

But why does it matter so much?

Why accounts receivable matters so much for your business

Accounts receivable directly decides whether you have enough cash to pay rent, run payroll, and keep operations going next month.

When customers take longer to pay, your cash gets delayed. When cash gets delayed, you still have to cover expenses on time. That creates a gap. If that gap grows, you start relying on reserves, short-term debt, or delaying your own payments. That’s how a slow collection cycle turns into a real financial problem.

The SBA’s financial management guide is a good starting point if you want to build stronger financial habits across your business.

I’d argue this is one of the most underestimated problems in small businesses. The Federal Reserve’s 2024 Small Business Credit Survey found that 51% of small businesses cite uneven cash flows as a top financial challenge.

Sales are happening. The money just isn’t showing up fast enough.

This is why I always tell founders that forecasting revenue isn’t enough. You need to estimate when that revenue will actually be converted into cash. That’s where AR assumptions feed directly into your cash flow forecast, and tools like our cash flow calculator can give you a quick read on where you actually stand.

Assuming that you will receive a payment in 30 days, whereas the actual situation is more like in 45 days, your whole cash position will change. That is what it takes to remain afloat and consistently scramble to meet bills.

Need to develop a cash flow forecast to consider your AR timing? Try Upmetrics’ cash flow forecasting feature to map out exactly when revenue turns into cash.

How can you manage or improve accounts receivable?

Major AR issues are due to ambiguous terms, delayed payments, or non-follow-ups. Fixing them typically makes a larger impact than any tool or software.

I’d focus on these five areas first:

1) Set clear payment terms upfront

Don’t leave this until after the work is done. Define terms in writing before the sale or project begins. Whether it’s Net 30, Net 15, or due on receipt, the expectation should be documented and agreed upon before the invoice is ever sent.

2) Invoice immediately after delivery

Timing matters more than most people think. If you wait a few days to send an invoice, you’ve already delayed your own payment cycle. Sending it the same day or next business day keeps things moving.

3) Follow up with a system, not memory

Late payments happen because no one follows up on time. I’d keep it simple: a reminder before the due date, a follow-up on the due date, and another check-in a week after. Most payments come in after the first or second nudge.

4) Use aging reports to stay ahead

An accounts receivable aging report organizes your outstanding invoices into time buckets:

- Current

- 1 to 30 days past due

- 31 to 60 days

- 61 to 90 days

- 90 days or more

A quick look at your aging report tells you exactly where to focus your follow-up efforts, instead of treating a two-day-late invoice the same as one that’s been outstanding for three months.

5) Consider small incentives for faster payment

For larger invoices, offering a small early-payment discount can bring cash in sooner. Giving up 1-2% is often worth reducing the wait by a few weeks.

How AR shows up on your financial statements

Accounts receivable show up across all three of your core financial statements, each telling a different part of the story.

On the balance sheet, accounts receivable appear under current assets. It represents money your business expects to receive soon. If your AR is growing, your assets are increasing on paper, but that doesn’t mean your cash has increased.

On the income statement, AR shows up indirectly through revenue. The moment you make a credit sale, the revenue is recorded even though no cash has been collected yet. This is why your profit can look strong while your bank balance stays flat.

The cash flow statement is where the difference becomes clear. If your accounts receivable increase during a period, it reduces your operating cash flow. That’s because more of your revenue is still tied up in unpaid invoices. If AR decreases, it means you’re collecting cash, which improves your cash flow.

All three statements are connected, but they don’t move at the same time. Revenue moves first, receivables sit in between, and cash comes last.

I always recommend looking at all three together. Strong revenue with rising receivables and weak cash flow is a signal that collection, not sales, is the issue. That’s a distinction that matters when you’re putting together the financial section of your business plan.

Once you understand how AR flows through your statements, the next question is obvious: how do you actually measure it?

Key AR metrics (Turnover + DSO + benchmarks)

If you look at your total receivables balance, it won’t tell you much. A better question would be how fast are you collecting it. There are two metrics that answer that directly:

- accounts receivable turnover

- days sales outstanding (DSO)

Accounts receivable turnover ratio

This tells you how many times you collect your receivables in a given period.

Formula: Accounts Receivable Turnover = Net Credit Sales ÷ Average Accounts Receivable

Example: If your annual credit sales are $120,000 and your average AR is $12,000, your turnover is 10. That means you collect your receivables about 10 times a year, or roughly once every 36 days.

A higher turnover means you’re collecting faster. A lower number means cash is sitting longer with customers. I’d watch this number closely if your terms are Net 30, but your turnover implies 45-60 days. It means something is slipping in your process.

Days sales outstanding (DSO)

DSO translates that ratio into days, which is easier to interpret.

Formula: DSO = 365 ÷ accounts receivable turnover

Example: 365 ÷ 10 = 36.5 days. On average, it takes you about 36 days to get paid.

If your DSO is higher than your payment terms, you’re effectively extending credit without intending to.

So, what’s a good DSO? It depends on your industry, but here are typical ranges:

| Industry | Typical DSO | What it means |

| Retail | ~5 days | Mostly cash or card, minimal credit |

| B2B Wholesale/Retail | ~30 days | Invoice-based, short credit terms |

| SaaS | ~45 days | Moderate billing cycles |

| Manufacturing | ~50 days | Longer invoicing cycles |

| Professional Services | ~55 days | Slower, relationship-driven |

Though these aren’t strict targets, they give you a baseline. The key is consistency. If your DSO starts rising over time, it usually points to delayed invoicing, weaker follow-ups, or changing customer behavior.

A rough rule: if your DSO exceeds your stated payment terms by more than 15-20%, your collection process is slipping. For example, if you’re on Net 30 terms but your DSO is sitting at 40 days or more, that’s worth investigating

At a practical level, DSO answers one question: how long your money stays out of your business after you’ve earned it. Most of the time, a high DSO means slow payments. But occasionally, a customer doesn’t pay at all. That’s a different problem, and it needs a different response.

What happens when customers don’t pay?

Some invoices don’t get paid on time. A few won’t get paid at all. It is not whether this will occur, but how you will cope whenever this occurs.

A majority of the cases take a foreseeable route:

- Begin with a friendly reminder during or on the deadline.

- Send a more firm follow up message in case of no reply.

- Give a formal notice with a hard deadline in the event of them going silent.

- Decide whether to escalate to a collections agency or write it off and move on

The mistake most businesses make is sitting too long at each stage. One unpaid invoice can quietly drag on for months if nobody draws a line.

The way I think about it is time vs value. When the amount is small, it is not usually worth much pain. When it is huge, then escalation should occur sooner. Either way, set a cutoff point so one invoice doesn’t drag on for 90 days. Otherwise, receivables stop being assets.

Assume a small slice of your AR won’t get collected. That’s exactly why businesses set aside an allowance for doubtful accounts. It keeps your numbers honest and means you’re not caught off guard when a payment never comes in.

When you’re confident a payment won’t come in, it’s written off as bad debt. That removes it from accounts receivable and records it as an expense. The IRS allows this as a deduction, but only if the income was previously recorded.

Before we get into how to forecast, let me distinguish between accounts receivable and accounts payable.

Accounts receivable vs. accounts payable

If accounts receivable are money coming in, accounts payable are money going out. They’re not separate ideas. They operate at the same time in every business.

Most confusion starts here. I get it, though. You’re waiting on customers to pay you, while you also have bills to pay vendors. Accounts receivable is what you’re owed. Accounts payable is what you owe. The problem is, these two don’t move in sync.

| Feature | Accounts Receivable (AR) | Accounts Payable (AP) |

| Definition | Money owed to your business | Money your business owes others |

| Balance Sheet Position | Current Asset | Current Liability |

| Normal Balance | Debit | Credit |

| Example | Client invoice for $5,000 | Vendor bill for $2,000 |

| Impact on Cash Flow | Delays cash coming in | Delays cash going out |

AR and AP define your timing gap. If your customers take 30 days to pay but your vendors expect payment in 15 days, you’re funding that gap out of your own cash.

That’s why a business can grow and still feel cash pressure. Revenue comes in slowly through receivables, while expenses go out faster through payables.

If I’m running a business, I’d focus less on managing one side and more on controlling both sides together. Collect as quickly as possible while using your payment terms without damaging relationships. That balance keeps your cash flow stable.

That balance matters more than most founders realize, and the numbers back it up.

Spreadsheets are exhausting & time-consuming

Build a cash flow forecast that ties AR to AP

How to forecast accounts receivable

At a basic level, you’re estimating how long customers take to pay you and applying that delay to your revenue. If you sell on Net 30 but customers usually pay in 45 days, part of your revenue will always be stuck as receivables. The relationship is simple:

- Faster collections → less cash tied up in invoices

- Slower collections → more cash locked up, longer

When you are new, base your anticipated terms of payment. However, customers tend to make their payments later than promised. I always suggest planning with a buffer. On paper, Net 30 tends to act the same as 40-45 days on the ground.

Here’s a simple formula that can be used to estimate your projected AR at any time:

Projected AR = (Projected Revenue x% of Credit Sales)x(Average Collection Period/365).

For example, say you project $100,000 in quarterly revenue, 60% of it on credit terms, and your average collection period is 45 days. Your projected AR would be around $7,397. That’s money you’ve already earned but won’t see in your bank account until those invoices are paid.

This is important because it’s where most cash flow gaps come from. If you’re new to financial forecasting, understanding how AR fits into your projections is one of the most practical places to start

The goal isn’t precision. It’s visibility, as you want a realistic estimate of how much revenue will still be waiting to be paid at any point in time. That’s what helps you add accounts receivable and accounts payable to your forecast and build a cash flow projection that actually reflects reality.

Manage and track accounts receivable in Upmetrics

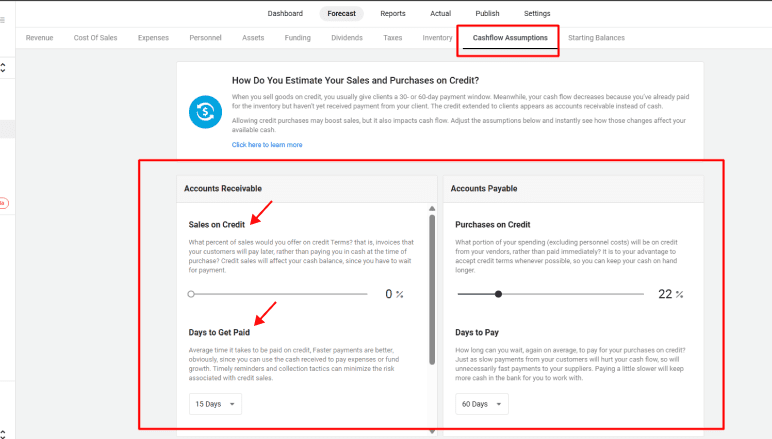

If you’re building a business plan or financial forecast, your AR assumptions need to be connected to the rest of your numbers, not sitting in a separate spreadsheet that you update manually.

Upmetrics has a dedicated Cashflow Assumptions tab inside the Forecast builder, where you can set up your accounts receivable details alongside your payables.

Forecasting accounts receivable

Under the Accounts Receivable section, you’ll find two inputs:

- Sales on Credit: the percentage of your sales that customers will pay later rather than upfront

- Days to Get Paid: the average number of days it takes to collect payment on those credit sales

Adjust both based on how your business actually operates. These assumptions feed directly into your cash flow projections, so any change you make is instantly reflected across your financial model.

Tracking accounts receivable

Once your assumptions are in place, Upmetrics automatically generates separate receivable and payable reports available under the Reports section. These are broken down into monthly, quarterly, and yearly views, giving you a clear picture of how much revenue is still unpaid at any point in time.

![]()

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.