Many small business owners and first-time founders think COGS and direct costs are the same thing. They’re not. COGS (Cost of Goods Sold) is what all your direct costs add up to for the stuff you actually sold during a period.

So what counts as a direct cost? That’s where most people get stuck. Is your own time a direct cost? What about shipping, the freelancer, or the Canva subscription you only use for product labels?

In this guide, I’ll explain what is direct cost, how it relates to COGS, examples for product and service businesses, a formula you can actually use, and the four mistakes founders make most often.

What is a direct cost?

A direct cost is any expense you can trace directly to the product, service, or project it helped produce. The three most common types are:

- Direct materials: the raw inputs that physically go into the product or are used up delivering the service.

- Direct labor: the wages you pay for the time spent making that product or delivering that service.

- Directly tied supplies or equipment: consumables or tools used specifically on that one product, project, or client.

I’ll break each of these down with real product and service examples further below.

How do you tell if a cost is direct?

Here’s the test that resolves most of the confusion: if you stopped making this specific product or delivering this specific service tomorrow, would this cost go away?

If the answer is yes, it’s a direct cost. If the cost sticks around regardless, it’s not.

For example, in a candle business, the wax used for a batch of candles is a direct cost. No candles, no wax purchase. But the electricity for the workshop continues whether you produce a few candles or many, so that isn’t a direct cost.

How does a direct cost relate to COGS?

As explained earlier, a direct cost is the cost of making one specific thing. COGS is the total of those costs for everything you actually sold during a period.

Say you sell candles. The direct cost of making one candle is $6.66. If you sold 200 candles in March, your COGS for March is 200 × $6.66 = $1,332.

The catch: direct costs only become COGS when the product is sold.

If you bought $5,000 of wax in March but only sold candles made from $1,200 of it, only $1,200 hits your COGS for March. The rest sits on your balance sheet as inventory until those candles sell.

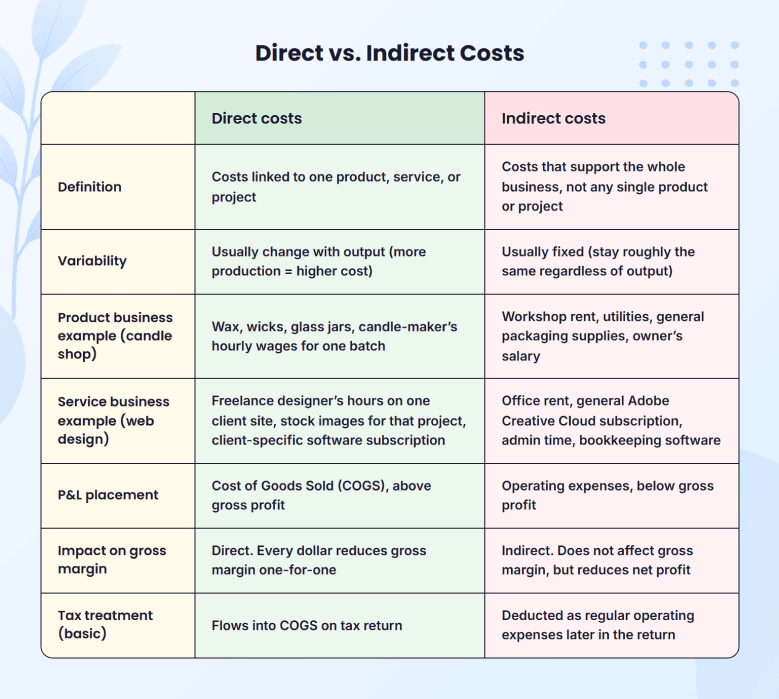

Direct costs vs. indirect costs: what’s the difference?

Direct costs are tied to one specific thing. Indirect costs support the business as a whole.

A direct cost happens only because you made a product or delivered a service. If that product or service didn’t exist, the cost wouldn’t exist either.

An indirect cost exists simply because the business is running. Think rent, utilities, accounting software, or the laptop used for daily work.

(If you’re looking for direct vs. indirect in cash flow statements, that is a separate topic covered under direct vs indirect cash flow methods.)

The biggest confusion comes from shared-use costs. Utilities, tools, shipping, and subscriptions may feel tied to a product, but if they are used across the business, they are indirect.

Types of direct costs with real examples

Most direct costs fall into three buckets:

- Direct materials

- Direct labor

- Directly tied supplies or equipment

Each one looks different for a product business versus a service business, so I’ll show both side by side under each type.

Direct materials

As introduced earlier, direct materials are the raw inputs that physically go into a product, or are fully used up delivering a service.

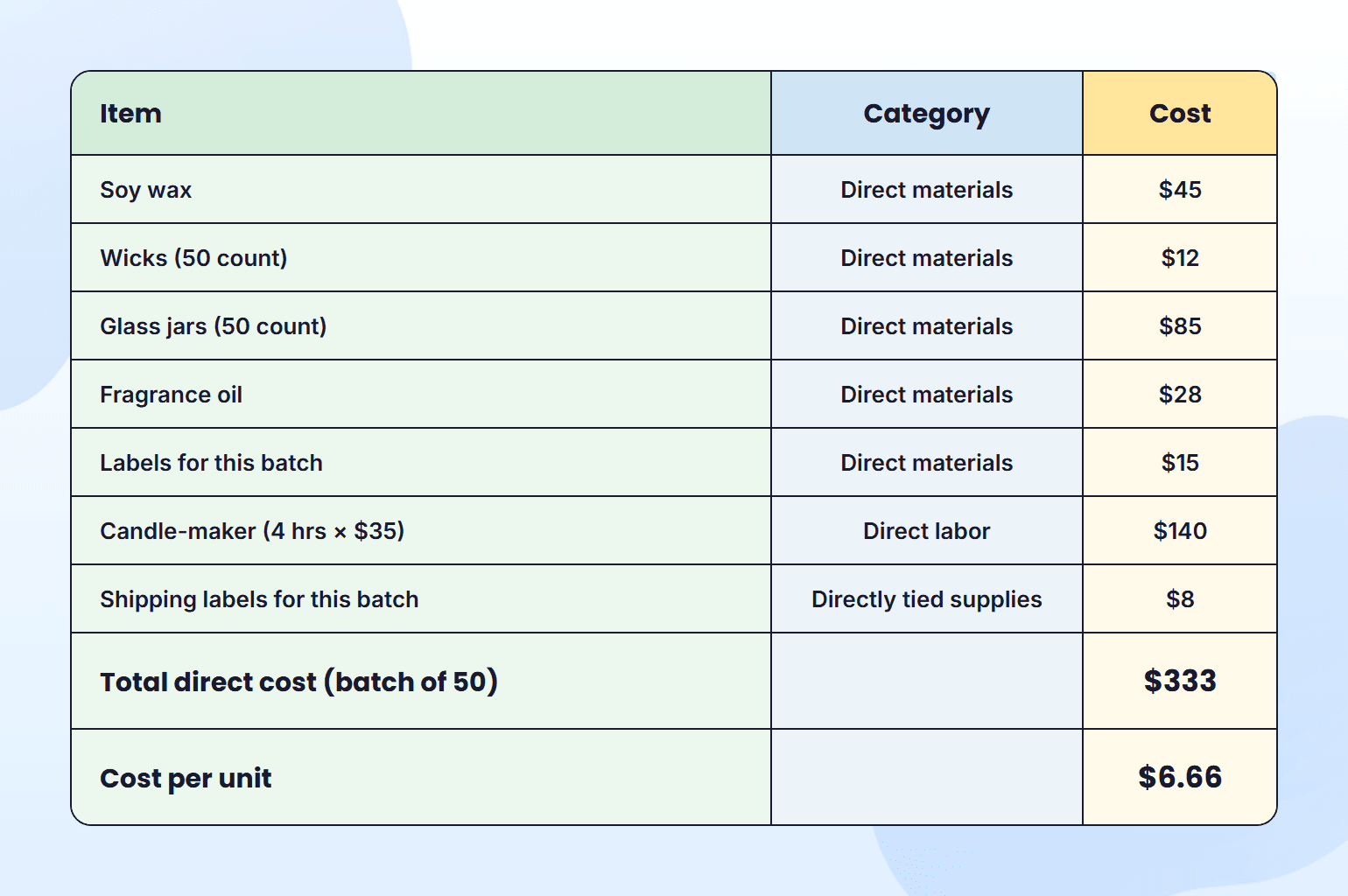

Product example: a candle business. For one batch of 50 candles, direct materials might include:

| Item | Cost |

| Soy wax | $45 |

| Wicks (pre-tabbed, 50 count) | $12 |

| Glass jars (8 oz, 50 count) | $85 |

| Fragrance oil | $28 |

| Labels printed for this specific batch | $15 |

All of it physically becomes the product. If you didn’t make this batch, you wouldn’t buy any of it.

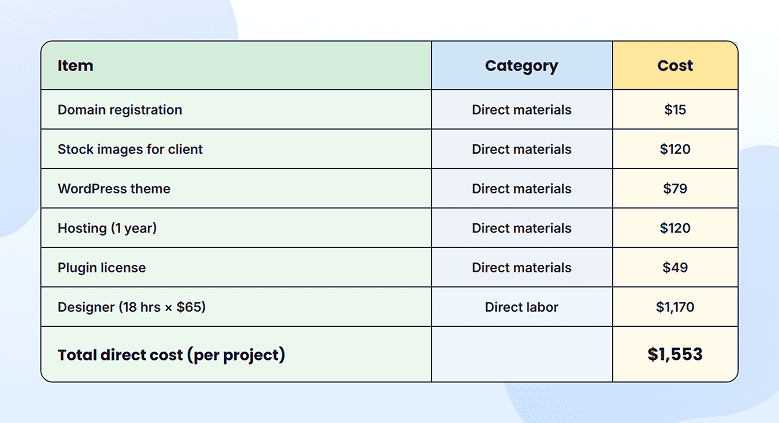

Service example: a website design project. For a single client build, direct materials might include the custom domain registration ($15), stock imagery licensed specifically for their site ($120), and a premium WordPress theme you bought just for this project ($79).

Direct labor

Direct labor is the money you pay for work done on a specific product or a specific client’s job. This includes wages, plus taxes and benefits.

For a realistic benchmark, BLS data puts average private-sector compensation at $46.15 per hour, $32.36 in wages, and $13.79 in benefits. So when you calculate direct labor, you’re not just using the hourly wage; you’re using the fully loaded rate.

Product example: a candle business.

- A candle-maker spends 4 hours making a batch of 50 candles

- Hourly wage: $25

- Total hourly cost (wage + taxes + benefits): ~$35

- Direct labor for the batch: $140

Service example: a website design project.

- A freelance designer spends 18 hours on one client’s website

- Rate: $65 per hour

- Direct labor for the project: $1,170

The 3 hours she spent on internal admin the same week? Not direct, those hours don’t belong to any specific client.

Does the owner’s salary count as direct labor?

Almost never. If you’re a salaried owner, your compensation is indirect. The only exception is when you pay yourself hourly for measurable, billable work on a specific product or project, and track those hours cleanly.

Most owners do not do this, which is why their salary is treated as an operating expense, not part of COGS.

Equipment and supplies tied to output

This category includes materials, small tools, or items used only for one product, one project, or one client. It does not include general office supplies or tools used across the business.

| Product example (candle business) | Service example (website design project) |

| Custom mold for one candle line | Plugin license for one client’s website |

| Color dye for one batch | Stock video subscription used for one project and then cancelled |

| Shipping labels for a specific set of orders | Shipping costs for brochures for one client |

The test is the same as before: if the cost exists only because of one product, project, or client, it is a direct cost. If the same item is used across multiple jobs, it is an indirect cost, even if one job uses it more.

How to calculate direct costs?

Calculating direct costs is addition, not algebra. The formula is the same for every business:

Direct Cost = Direct Materials + Direct Labor + Directly Tied Supplies or Equipment

Always calculate this for one product, one project, or one client at a time. Not for the whole month.

Calculate direct costs for a product business

Using the same candle example from above, you add up all the costs for one batch of 50 candles.

That $6.66 is the number the candle-maker uses to set a price.

Calculate direct costs for a service business

Using the same website design example, you add up all the costs for one client project.

In service businesses, labor is usually the highest cost. Here, $1,170 is about 75% of the total. That is normal.

Once you know your direct cost per unit or per project, use our free markup calculator to set a price that hits your target gross margin.

Why direct costs matter for pricing and gross margin?

Direct costs don’t just fill in a line on your P&L. They decide whether your business has a gross margin to work with at all.

The chain is simple:

- Revenue − Direct Costs (COGS) = Gross Profit

- Gross Profit / Revenue = Gross Margin %.

Take the candle business example from earlier. It sells for $20, the direct cost is $6.66, gross profit is $13.34. That’s a 66.7% margin.

Now imagine material costs or wages increase, and the cost per candle goes up to $10. The price is still $20, but the profit drops to $10. The margin falls to 50%. A small change in cost leads to a big drop in margin.

Gross margin is the pool that covers everything else: rent, insurance, software, your paycheck, taxes, and profit.

If you sell 1,000 candles a month, a $3.34 drop per candle means $3,340 less available to run the business. This directly affects cash flow forecasting and planning.

Most founders don’t lose margin because direct costs went up. They lose it because they classified costs incorrectly.

Model direct cost & margin shifts in real time

Why classification matters to the IRS and your bank?

Direct cost classification isn’t just internal bookkeeping. Two outside parties care a lot about how you do it, and both of them have leverage over your business.

How the IRS sees direct costs

If you sell anything (products or services), you report COGS on your tax return. Understating your direct costs makes your gross profit look higher than it is, and you pay more income tax than you owe.

Overstating them does the opposite, and that’s the kind of error that draws IRS attention if you’re ever audited.

How your bank sees direct costs

When you apply for a loan or line of credit, the lender looks at your gross profit and gross margin first. If your direct costs are misclassified, those numbers are wrong.

A margin that looks too low makes you look unprofitable. A margin that looks too high makes the bank question your books. Either way, your loan application gets weaker.

Common mistakes founders make when tracking direct costs

These four mistakes show up in most small business P&Ls. Even one of them can quietly damage your gross margin.

1. Treating the owner’s salary as direct labor

As explained earlier, unless you pay yourself hourly for specific, tracked work, your pay is indirect. If you count it as direct, your COGS goes up, and your margin looks lower than it really is.

2. Allocating rent or utilities as direct costs

Rent and utilities support the whole business, not one product. Trying to split them across products makes your margins look worse and leads to pricing based on the wrong numbers.

3. Misclassifying shipping

Shipping has two sides, and they don’t belong in the same place.

- Shipping a finished product to a customer is a direct cost for that order.

- Shipping that brings raw materials to you is part of what those materials cost.

Mixing both together throws off your margins and your tax reporting.

4. Counting all inventory as a direct cost when you buy it

Inventory is not a cost when you buy it. It becomes a cost only when you sell it. If you buy $5,000 of materials but use $1,200, only $1,200 should show up that month. The rest stays as inventory.

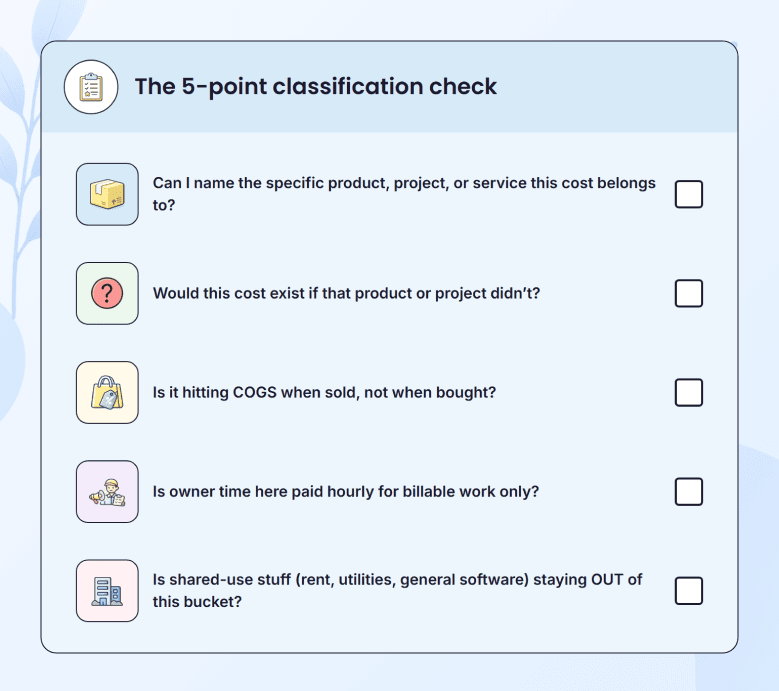

When these mistakes add up, they don’t just affect margins. They create cash flow problems that show up later. Use the check below before you add any cost to your direct cost bucket.

If any answer is “no” or “not sure,” the cost probably doesn’t belong in direct costs.

Conclusion

Getting direct costs right takes a bit of practice, but it’s worth it. You end up with accurate margins, cleaner books, and pricing you can actually trust.

The simplest test is all you need to remember. For any cost, ask: if you stopped making this product or delivering this service tomorrow, would this cost go away? If yes, it’s a direct cost. If no, it’s not.

From here, work out your direct costs per unit or per project, check they match what shows up on your P&L, and use those numbers to set your pricing.

Getting this right is the base for every pricing and margin decision, and the easiest way to do it is alongside your revenue projections, not separately. You can map both in our business plan builder.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.