Wouldn’t it be great if writing a business plan automatically meant you were ready to get funded? It doesn’t, and the reason is that lenders aren’t really reading the plan you wrote. They’re reading it for specific answers to questions you may not even know they’re asking.

I’ve sat on both sides of this. The plans that get funded aren’t always the best-written ones. They’re the ones that answer the specific questions a lender or investor is already asking before they open the doc.

Let’s see what lenders and investors really look for in a business plan.

Business history and operating track record

A lender doesn’t really read this section for history. They’re reading it for proof of operator behavior, evidence that you’ve been tested and made reasonable calls when it counted.

What they’re scanning for is pretty simple: when the business began, how revenue has changed, and whether there’s any sign of decision-making under pressure. The third one carries the most weight by a long way.

Here’s the rule underwriters work with, even if they don’t say it out loud: if I can’t see how you handled a setback, I assume you haven’t. And that assumption rarely gets revisited later.

So the worst version of this section isn’t one with bad numbers, it’s one with no friction in it at all. Clean, linear growth with nothing explained reads as either inexperience or omission, and both are risk signals.

The difference between a weak and a strong version is usually visible in just a couple of paragraphs.

- Weak: “Founded in 2021, the business has grown steadily, reaching $480K in revenue by year three. The team is committed to continued growth.”

- Strong: “We launched in 2021 and hit $180K in year one. In year two, we lost our largest customer, who was 28% of revenue, when they got acquired. We replaced that revenue in seven months by shifting from one-off projects to retainers, and closed year two at $310K. Retainers now make up 60% of our revenue, which is why year three came in at $480K with much lower volatility.”

It’s the same business with the same numbers, but the strong version actually proves an operator was at the wheel.

If you’re pre-revenue, the bar shifts, but the question doesn’t change. The strongest substitutes are operating roles where you owned a P&L of similar scale, or a paid pilot with real customers.

The weakest are general management roles with no scope detail, or unpaid pilots with friends and family. If your substitute looks more like the second list, this section won’t carry the weight a lender needs it to.

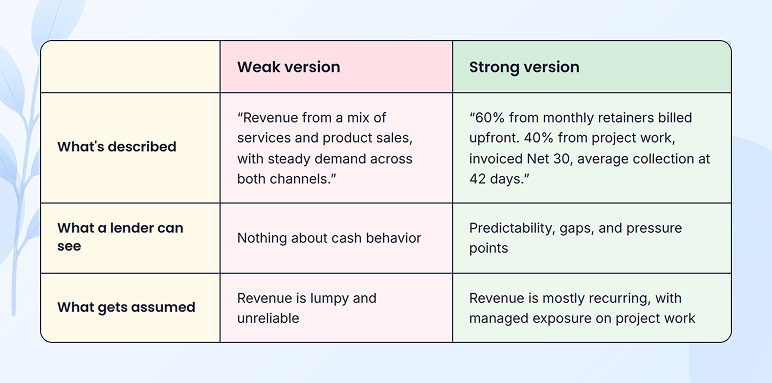

Revenue model: how the business actually makes money

Every dollar a lender gives you has to come back, and this section is where they check how that actually happens.

A lender isn’t reading this for positioning or value statements; they’re reading it for mechanics. Specifically, four things:

- What you’re actually selling (the product, the service, the unit of value)

- How it’s priced (one-time, subscription, retainer, per-unit)

- How customers pay (card on file, invoice, prepay, financing)

- When the cash actually lands (sales cycle length, payment terms, average days to collect)

The simplest test is this: Can the lenders trace a single dollar from sale to bank deposit? If that path isn’t clear, discount the revenue because the timing and reliability aren’t real.

The common version of this section stops at something like “we generate revenue through services” or “we sell products online.” That tells a lender almost nothing about cash behavior. A strong version breaks the same business down so the mechanics are visible at a glance.

This is also where strong sales can still create weak cash flow. If collections lag or receivables build up, growth on paper turns into a cash strain in practice. If your model has delayed payments built in, you have to show how that gap gets managed.

If you’re pre-revenue, there’s no collection history yet, so the mechanics you describe are the whole section. The catch is that a lender and an investor will read the same paragraph and walk away with different conclusions.

A lender wants to see validated payment terms, proof that customers will actually pay when you ask them to. An investor wants to see pricing power, whether those first customers are paying a price that can hold as you scale. If your plan only speaks to one, you’re telegraphing which audience you were writing for.

The management team behind the plan

A lender isn’t really funding a résumé; they’re funding execution. So this section is where they decide whether the people behind the plan can actually run the business that’s described in it.

The mistake the majority of founders make is writing this section like a LinkedIn page. Years of experience, company names, broad credentials. None of those answers the question a lender is actually asking, which is much narrower.

The question is this: for each thing this business needs to do in the next two years, can someone on this team prove they’ve already done it?

Lenders won’t write that question down anywhere, and they won’t run it as a formal exercise. But it’s the underlying judgment they’re forming as they read your bios, your resumes, and your personal financial statement. The fastest way to make sure your section answers that judgment is to build the mapping yourself before they have to.

Take a small commercial cleaning business applying for a $250K SBA loan. The mapping might look like this:

| What the plan needs the team to do | Receipt that satisfies a lender |

| Win and retain commercial accounts | Founder previously ran a regional account team and grew the book from $400K to $1.1M over three years |

| Manage 12+ hourly staff across multiple sites | Operations lead managed a 20-person crew at a previous facilities company |

| Hold gross margin above 38% as the team scales | Currently held at 41% over the past two years on the existing book |

| Stay current on payroll, insurance, and bonding | CPA-prepared books for the past three years, no late filings |

Every row that has a clean receipt reduces risk for the lender. Every row that’s empty or vague is a question they’ll ask in underwriting, or worse, an assumption they’ll make against you.

Gaps are normal. If the operations role isn’t filled yet, name it and say what you’re doing about it. A lender finding the gap themselves is much worse than you naming it first.

If you’re a solo founder, the same exercise still works. The receipts just have to come from somewhere else, prior roles, smaller ventures, or projects where you owned the outcome end-to-end.

Market opportunity and competitive positioning

A lender’s read of this section comes down to a pretty narrow question: is there enough demand, in the place you actually operate, to keep this business running for the term of the loan?

In my experience, that’s a smaller question than what founders write to. The instinct is to lead with a big industry number, the kind that signals ambition. The problem is that a TAM figure doesn’t tell a lender anything about your demand.

Your demand lives in a much smaller circle, the customers you can actually reach, in the geography you actually operate in, with the channels you actually have. That’s the only number a lender can lend against.

So I’d push every founder to do two things here.

- Show the reachable customer count

- Show how those customers are already being acquired

Something like this lands well:

“We serve independent gyms within a 20-mile radius of our facility, around 180 locations. We currently sign new accounts through partnerships with two equipment service companies and referrals from existing customers, converting roughly one in five qualified leads.”

An investor reading the same paragraph will conclude the business is too small to back because the question they’re asking is different.

A lender is asking, “Is there enough here to cover three to seven years of payments? An investor is asking, “How big can this become if it works? A 180-gym circle answers the first question beautifully and fails the second one completely.

So if you’re writing for both audiences, you need two layers in this section. The reachable circle that makes a lender comfortable. And above it, a credible path from that circle to something much bigger, adjacent geographies, adjacent customer types, a product extension, or a channel expansion.

The lender reads the first layer and stops, and the investor reads both and decides whether the second layer is plausible.

Competitive positioning works the same way. A lender wants to know you can hold your reachable customers against whoever else is trying to serve them. An investor wants to know what protects you once you’ve won: switching costs, network effects, brand, and distribution lock-in.

Apart from that, always make sure that wherever you cite a market size or growth rate, source it from somewhere a lender already trusts, the U.S. Census, BLS, an IBISWorld summary, or a relevant trade association.

Solid market research for your plan costs nothing to add and lifts the credibility of every other claim in the section. The Federal Reserve’s Small Business Credit Survey consistently shows cash flow and market weakness as two of the top reasons applicants get denied.

Historical financials and debt service coverage

If a loan file is going to die, it comes down to one number that’s either missing, calculated wrong, or sitting just under the line.

That number is the debt service coverage ratio, or DSCR. It’s the metric that tells a lender whether your business actually throws off enough cash to cover the loan you’re asking for.

The standard formula is:

DSCR = Net Operating Income ÷ Total Annual Debt Service

Lenders reconstruct NOI from your tax return or financials by adding depreciation, amortization, and interest back to net income, since depreciation and amortization aren’t real cash costs and interest is already captured in the denominator. That add-back step happens before the DSCR ratio gets calculated.

There are actually two DSCR numbers to know here, and they’re often confused. Per current SBA underwriting guidance, the written floor under SOP 50 10 8 is a 1.15x global DSCR for 7(a) loans, meaning your business generates $1.15 in cash for every $1.00 of debt service.

That’s the regulatory minimum, and it’s lower than most founders assume. But in practice, most SBA and conventional lenders underwrite to 1.25x as internal policy, and some push for 1.5x if your industry is on the riskier side.

So your file can technically clear the SBA’s bar and still get declined by the bank, because the bank’s threshold is set higher than the SBA’s. A DSCR that falls between 1.15x and 1.25x is one of the common reasons SBA loans get denied, even when founders assume they’re safely over the minimum. It’s worth running the math honestly before you submit, and knowing which number your specific lender is working with.

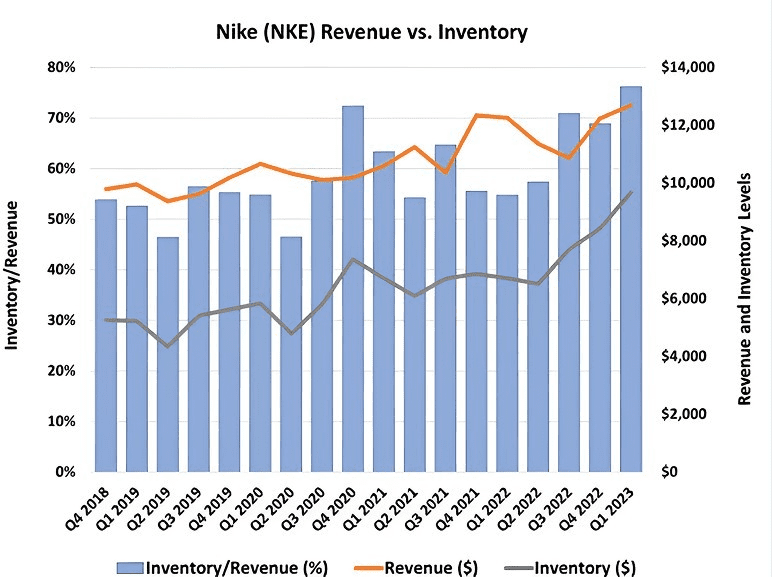

Any business can get caught in the same trap: revenue stays healthy on paper while cash timing breaks down. A company the size of Nike can absorb a quarter or two of that kind of dislocation, though not without a market reaction. When the company’s quarterly inventory jumped 44% year-over-year to $9.7 billion in 2022, and the earnings release triggered margin warnings, the share closed about 10% lower the following day.

A small business applying for a $300K SBA loan has no equivalent buffer. That’s why lenders underwrite to cash coverage in the first place, not to revenue, and it’s what makes the DSCR ratio load-bearing for a decision the rest of the plan can’t override.

Tired of digging through spreadsheets to calculate DSCR?

Auto-build the financials a lender actually wants

Forward projections: with and without funding

If your projections look the same with or without the loan, there’s no reason to fund you.

Usually, founders write financial projections as a prediction. In my view, a lender reads them as an argument, what changes because of this money, and does that change actually justify the risk?

An investor reads the same projections as something else entirely, a hypothesis about what this business becomes at scale. The lender is looking for a floor. The investor is looking for a ceiling. Most founders write one and call it done.

Three things get checked, regardless of which reader is in the seat.

- First, two clear scenarios on the same page, one showing the business on its current path, the other showing what the loan unlocks. If the difference isn’t visible, the assumption is that the capital isn’t essential.

- Second, traceable assumptions. Every number comes from somewhere: pricing, volume, hiring pace, conversion rates. If a lender can’t follow how you got there, they won’t trust the output. If an investor can’t follow it, they’ll assume you back-solved the numbers to hit a valuation, which is one of the fastest ways to lose credibility in a room.

- Third, the downside. Plans showing only a best-case signal inexperience, and understanding how investors really read your projections, are often what separates a fundable plan from a rejected one. Model what happens if revenue comes in 15-20% below base.

If you’re pre-revenue and building these from scratch, both audiences accept that everything is estimated, but they lean harder on assumptions than on outputs. Cite the source for every key input, industry benchmarks, comparable businesses, signed letters of intent, and anything that makes the number credible.

Collateral and available assets

Until now, your plan has argued that the business will repay the loan. This section answers a different question: what happens if it doesn’t. That’s what collateral is for. It isn’t the primary decision driver, but it becomes important the moment cash flow looks uncertain.

The first mistake I see is listing assets at the purchase price. That’s not how lenders think. Look at what those assets would sell for today under pressure. Equipment, especially major equipment and asset purchases that are financed or specialized, is often discounted to 50-70% of its resale value. Inventory is even lower. Real estate holds up better. If your numbers don’t reflect that reality, adjust them down immediately.

The bigger question founders have is what happens if collateral is thin. In SBA-backed loans, collateral supports the decision, but it doesn’t make it. Strong cash flow can compensate for weaker collateral. Weak collateral plus unclear financials is what raises real risk.

The purpose of the loan (or investment)

A lender isn’t really funding “growth.” They’re funding specific things that produce specific outcomes, and this section is where that gets proven.

The question is what exactly the money is for, and why that amount. The first filter I’d apply is precision. “Working capital” on its own doesn’t tell a lender much; they want to see what that actually breaks into. Something like:

- Payroll for a defined number of months

- Equipment or capex tied to a specific capacity or efficiency gain

- Inventory sized to a demand forecast you’ve already shown

- Receivables gap coverage with a clear window (e.g., 60 days)

- Marketing or launch spend tied to a specific channel or campaign

The clearer each line is, the easier it is to justify the total. Round numbers without backing, in my experience, get questioned or reduced almost automatically.

The second check is linkage. Every dollar requested should tie back to an outcome the plan has already described:

- Equipment → capacity or efficiency

- Hiring → revenue the new role generates

- Inventory → demand you’ve already forecasted

- Marketing → a channel with a conversion rate attached

If I can’t see what a line item actually changes in the business, I assume it’s padded, and padded lines get trimmed or denied outright.

Estimates are fine; almost all the numbers in this section are estimates anyway. What lenders actually push back on are estimates without any backing. A vendor quote, a contractor estimate, or a historical bill from a previous vendor turns a guess into something defensible.

If you’re requesting funds to buy an existing business, the use-of-funds breakdown has to include purchase price, working capital at closing, and transition costs, each tied to the seller’s financials.

And if your use doesn’t map cleanly onto SBA categories, it’s worth looking at non-SBA lending options where the purpose-of-funds standards are more flexible.

Beyond the business plan, what else do they check

The plan opens the decision, but a parallel set of checks, most of them outside the document you’ve been building for weeks, actually closes it. In my experience, this stage is the underestimated part of the whole process.

The check I’d tell you to worry about first is personal. For small business loans, especially SBA-backed ones, the primary guarantor is as underwritten as the business. Personal credit score, repayment history, and overall financial position, all pulled early.

Under the updated SBA SOP 50 10 8 that took effect in 2025, the minimum FICO SBSS score is now 165, one of several collateral and credit changes introduced by the 2025 SBA policy update. I’ve watched strong plans get stalled because the guarantor’s credit sat a few points below that line.

The check I’d have you worry about next is verification. Tax returns, bank statements, and financial disclosures get matched against the numbers in your plan, and if they don’t line up, doubt spreads backwards into everything else you’ve written. My rule of thumb is if your plan says something a document can contradict, the document will win, every time.

And then there’s the long tail of required filings, personal financial statements, tax returns, resumes, background checks, and ownership disclosures. None of these is paperwork for paperwork’s sake. Each one is a small integrity check.

If you’re a first-time applicant or your deal has any complexity, a free SBDC business plan review or a lender-side packager can catch alignment issues before they reach underwriting. The Nav team has a useful explainer on how underwriters weigh the 5 Cs that’s worth reading alongside your draft.

Conclusion

A well-written plan doesn’t guarantee a yes. Even the cleanest section-by-section work can get declined for reasons outside what a plan can address, such as market conditions, lender appetite shifts, or a personal credit score that needs work first.

What a well-written plan does guarantee is that you’ll know why if it happens. A vague plan that gets declined leaves the founder wondering. A specific one that gets declined gives them something usable, an actual reason, an actual number, an actual gap. That’s not a small thing. It’s what makes the second application different from the first.

If you’d rather not build that structure from scratch, you can build a funding-ready business plan with Upmetrics, which has that structure built in by default.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.