Why does your business sometimes feel short on cash even when everything looks fine on paper?

In many cases, it comes down to timing. You’re receiving bills and recording expenses before payments actually go out. That gap sits on your balance sheet as accounts payable (AP), and I’ve noticed it’s one of the most overlooked parts of running a small business.

This blog breaks down how AP works, how to record it, and how to manage it without letting it drag your cash flow.

What is accounts payable?

Accounts payable is the money your business owes suppliers for goods or services you’ve already received but haven’t paid for yet. It comes from purchases made on credit, where the vendor gives you time, usually 30 to 90 days, before the payment is due.

If you’ve ever looked up the accounts payable definition and walked away more confused, here’s the easier version: if you’ve received the bill but the cash hasn’t left your account, that amount sits in accounts payable.

From an accounting point of view, AP is a current liability on your balance sheet. It represents short-term obligations your business needs to settle soon, and it only shows up for credit transactions, never for anything you pay for on the spot.

It also helps to separate accounts payable from similar terms that often get mixed up. Accrued expenses are expenses you’ve incurred but haven’t been billed for, such as salaries you owe at the end of the month.

Notes payable are loans with specific payment schedules and interest rates. Trade payables are sometimes used as a synonym for accounts payable, but often refer specifically to payables owed to suppliers, relating to inventory or key operations.

The kinds of bills that sit in your AP balance look like this:

- Rent and lease payments

- Utility bills (electricity, gas, internet, phone)

- SaaS and software subscriptions are billed on terms

- Contractor and freelancer invoices

- Inventory and supplies purchased on credit

- Professional services like legal, accounting, or consulting

- Shipping, freight, or logistics charges

- Marketing and advertising vendor invoices

If a purchase clears your card or bank account the same day you make it, it’s not AP. AP only covers bills that are paid later, on terms.

How accounts payable works

The moment a vendor sends you an invoice, accounts payable starts. You’ve already received the service or goods, so you record the expense immediately, even though you haven’t paid yet. That’s why your profit can change before your cash does.

From there, the invoice moves through a lifecycle. You check it against what you ordered and received, route it for approval, schedule the payment based on terms, and clear it once the payment goes out. Whether you formalize these steps or not, this happens every time you handle a bill.

This timing is where most confusion comes from. You might see expenses in your reports and assume cash has already gone out. It hasn’t. At the same time, those unpaid invoices are building up in the background. If you don’t track that balance closely, it’s easy to underestimate how much you actually owe at any point.

In my experience, the breakdown happens at approval. Even if the invoice is correct and ready, it sits waiting for someone to sign off. That delay stretches payment timelines without anyone actively deciding to delay, which is why businesses often miss due dates.

Before we get into the steps, I want to clear up a common mix-up: accounts payable vs. accounts receivable.

Accounts payable vs. accounts receivable

I think most confusion comes from looking at these in isolation. You see unpaid bills and unpaid invoices, but don’t connect how they interact.

Accounts payable is the money you owe vendors. Accounts receivable is the money customers owe you. One is a liability, the other is an asset.

Where it gets interesting is timing. Accounts receivable is how quickly cash is coming in. Accounts payable tells you how fast cash is going out. If it takes you 30 days to collect on an account but you have to pay a vendor in 15 days, you’re lending them money. That’s a prime cause of cash flow issues, despite otherwise good sales.

Let’s take a simple example. Say your AR is $40,000 on average 45-day terms, and your AP is $20,000 on 15-day terms. On the face of it, you’re owed twice as much as what you owe vendors. But you actually pay three times as quickly as you receive. You’re bankrolling the difference out of working capital every single month.

If I’m reviewing financials, I won’t just look at the balances. I’ll compare the timing. If receivables are stretching while clearing payables quickly, cash will tighten. If I can collect faster or negotiate longer payment terms, that pressure eases immediately. This is less about accounting and more about control over cash movement.

| Attribute | Accounts Payable (AP) | Accounts Receivable (AR) |

| Meaning | Money you owe vendors | The money customers owe you |

| Balance sheet | Current liability | Current asset |

| Debit/credit behavior | Increases with credit | Increases with debit |

| Responsible team | Bookkeeper / AP role | Billing/collections |

| Cash-flow impact | Delays cash outflow | Delays cash inflow |

A rough rule of thumb: if your average days-to-collect is more than 10 days longer than your average days-to-pay, you’re carrying the gap yourself. The bigger the spread, the more working capital you need just to stay flat. That’s the imbalance worth fixing first, before anything else on the AP or AR side.

One question I get asked constantly: if accounts payable represents money leaving the business, why isn’t it an expense? Even though I briefly mentioned it above, let me explain that properly.

Is accounts payable an asset or a liability?

Accounts payable are a current liability. It’s the money your business owes vendors for goods or services received on credit.

I think the classification matters more than it looks. Since AP sits under liabilities, it doesn’t reduce your profit when it appears; it increases what you owe. That’s why you can record an expense, see lower profit, and still have the same cash in your bank account. The obligation exists, but the payment hasn’t happened yet.

On your balance sheet, AP lives under current liabilities, usually due within 30 to 90 days. U.S. GAAP (set by FASB) treats it as a short-term obligation because you’re expected to settle it soon. If you’re building out your financials, that’s exactly where AP fits into the balance-sheet section of your financial plan.

I’d argue the biggest mistake businesses make is treating AP like an expense that’s already “handled.” It isn’t. Until you pay it, it’s still sitting there as a liability, and ignoring it is how businesses underestimate what they actually owe.

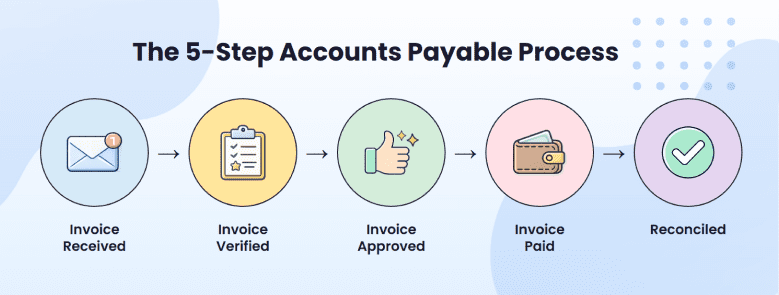

Once you know where AP sits on your books, the next question is what actually happens to an invoice between arrival and payment. Most small businesses run the same five steps, whether they’ve formalized them or not.

The accounts payable process: Step-by-step

Here’s what each step looks like when it’s working:

Step 1: Invoice received

As soon as you receive an invoice, log it the same day. The real issue with delays is visibility. If the invoice isn’t recorded, it doesn’t show up in your numbers, which means you’re operating without a clear view of what you owe.

That’s how early-payment discounts get missed, and due dates creep up unnoticed. By the time a vendor follows up, you will not get a choice of when to pay; you will be reacting to a deadline you failed to track.

Step 2: Invoice verified

Before you pay anything, confirm the invoice is correct. Match it against what you ordered and what you actually received. This will help you catch duplicate charges, pricing mismatches, and invoices for things you never received.

A $40 billing mistake doesn’t feel worth chasing, but thirty of them across a year is real money you’ve handed over for no reason. According to the AFP 2024 Payments Fraud and Control Survey, the majority of organizations report attempted or actual payments fraud in a given year, and verification is the first line of defense.

If you don’t verify invoices consistently, you won’t be able to control your outflows.

Three controls do most of the work in stopping AP fraud and errors:

- Three-way matching. Match the invoice to your purchase order and what was actually delivered. Quantity, price, and vendor all need to line up before payment goes out. This catches the bulk of duplicate invoices and inflated billings.

- Segregation of duties. Don’t let the same person enter, approve, and pay invoices. In small teams where that’s hard, the minimum is dual sign-off on anything above a set threshold (say $1,000). Even an informal second pair of eyes catches most internal fraud.

- Approval thresholds in writing. Document who can approve what at which dollar amount. Up to $500 with the bookkeeper, $500 to $5,000 with a manager, and above $5,000 with a founder. Without written rules, every invoice becomes a judgment call, and the controls erode.

Step 3: Invoice approved

When the invoice is approved, it’s sent to the person who’s responsible for that purchase, such as a founder, manager, or department head. You might think this is a small step, but it’s where the process gets bogged down.

There is nothing wrong with the invoice; it’s just waiting for approval in someone’s inbox. No one turns it down, no one sends a reminder, and before you know it, it’s past due.

The root cause is usually that no one owns approval speed. Approving invoices is just something that happens when the approver gets around to it. Without a rule on how fast that should happen (48 hours, one business day, whatever you set), the invoice ages until someone notices the due date.

Step 4: Invoice paid

After approval, you schedule the payment based on the agreed terms. You can pay early and capture discounts, or wait until the due date to keep cash in your business longer.

Founders tend to treat this as routine, but it directly affects your cash position. Paying everything immediately feels safe, but it reduces the cash you have available to run the business. Paying too late strains vendor relationships and adds late fees on top of the original invoice.

The math on early-payment discounts is usually worth running. A 2/10 net 30 discount works out to roughly 36% annualized return on the cash you use to pay early. If cash is tight, holding until the due date makes sense. If it isn’t, taking the discount almost always beats letting the cash sit.

Every payment either preserves cash or builds goodwill with vendors.

Step 5: Reconciled

Once the payment clears, you mark the invoice as paid and remove it from accounts payable. This step gets skipped more often than any other, and it causes the most confusion at month-end.

Until you reconcile, your books still show that you owe money even if the payment already went out, which is how businesses end up overstating what they owe.

Reconciliation is also your final check. Make sure that:

- The payment amount matches the invoice

- Nothing has been paid twice

- Nothing was left partially paid

- Your bank balance and books are in sync

Skipping this step isn’t an immediate disaster, but errors stack up by month-end.

To see the full process end-to-end, take a simple example. A small SaaS business receives a $1,200 AWS invoice on net 30 terms. The bookkeeper logs it the day it arrives, matches it to the AWS usage report, routes it to the founder for approval, schedules the ACH payment for day 28, and reconciles it the day after the bank transaction confirms. Same five steps, every time.

Now let’s see how that same AWS bill shows up in your actual books.

Accounts payable journal entries

You record accounts payable when you receive the invoice, not when you pay it. That’s how accrual accounting works. You recognize the expense when it happens, even if the cash leaves later. The IRS outlines this in Publication 538, which explains how accrual and cash methods treat expenses differently.

Let’s stay with the AWS bill from the previous section and watch it move through the ledger.

Entry 1: When you receive the invoice

You receive a $1,200 utility bill.

| Account | Debit ($) | Credit ($) |

| Utilities Expense | 1,200 | |

| Accounts Payable | 1,200 |

Your income statement now shows the $1,200 expense, which reduces profit. At the same time, your balance sheet shows a $1,200 liability under accounts payable. Cash hasn’t moved yet, but your obligations have increased.

Entry 2: When you pay the invoice

| Account | Debit ($) | Credit ($) |

| Accounts Payable | 1,200 | |

| Cash | 1,200 |

Now you’ve cleared the liability. Accounts payable go down, and cash leaves your account. This is the only point where your bank balance actually changes.

If you pay early and receive a 2/10 net 30 discount, the second entry changes slightly. You pay $1,176 in cash (2% off) and record the $24 difference as a purchase discount. The structure stays the same, only the amounts shift.

The order of these entries is what explains the profit-vs-cash gap. First, you recognize the cost and create the liability. Then you settle it. That gap between Entry 1 and Entry 2 is exactly why your profit and cash don’t move together.

Key accounts payable metrics to track

If accounts payable is a timing lever, these metrics tell you whether you’re using it well or letting it work against you. Looking at your AP balance alone won’t tell you much. You need to understand how fast it’s moving.

Three metrics give you the full picture:

1) Accounts payable turnover ratio

This tells you how often you pay off your suppliers over a period.

AP Turnover = Total supplier purchases ÷ Average accounts payable

Most accounting tools won’t show “total supplier purchases” as a clean line item. In practice, small businesses substitute COGS or total credit purchases instead. Either works as long as you stay consistent month to month.

A higher number means you’re paying faster. A lower number means you’re taking longer.

The mistake I see is assuming higher is always better. Paying too quickly can tighten your cash unnecessarily. This ratio only makes sense when you compare it to your agreed payment terms.

2) Days payable outstanding (DPO)

DPO converts your payment timing into days, which makes it easier to interpret.

DPO = (Average accounts payable ÷ Cost of goods sold) × 365

If your annual COGS is $600,000 and your average AP balance is $75,000, your DPO is (75,000 ÷ 600,000) × 365 = 45.6 days. On average, you take about 46 days to pay your vendors.

One caveat for service businesses: if your COGS is small (or close to zero, like in a service or SaaS business), this formula will overstate your DPO. In that case, swap COGS for total operating purchases or total expenses excluding payroll. The denominator needs to roughly reflect what you actually buy on credit; the number won’t tell you anything useful.

This is where most of your AP decisions actually come from. If your terms are net 30 but your DPO is 45, you’re effectively stretching payments beyond what you agreed to. That helps cash in the short term, but it can strain vendor trust if it becomes the norm.

Benchmarks vary by industry. Here’s a rough guide:

| Industry | Typical DPO |

| Retail | 20–30 days |

| B2B services | 30–45 days |

| Manufacturing | 45–60 days |

| Construction | 60–90 days |

| Healthcare | 45–75 days |

If you’re a new business without historical data, estimate DPO using your planned vendor terms plus a small buffer (net 30 usually behaves like 35 days in practice).

3) Cost per invoice

According to Levvel Research’s AP benchmark data, manual AP processing runs around $10 to $15 per invoice, while automated setups typically come in at $2 to $5. The APQC Open Standards Benchmarking study reports a similar spread, with top-performing teams processing invoices for under $2 each.

Cost per invoice = Total AP processing cost ÷ Number of invoices

This metric tells you how efficient your process is. What feels manageable at 20 invoices a month starts breaking at 200. Most small businesses don’t need to track this until volume crosses about 50 invoices a month.

If you’re only going to track one of these, track DPO. It gives you the clearest view of how long cash stays in your business before it goes out, and it’s the metric every vendor is quietly tracking about you.

You’ve seen how AP works and how to measure it. The next step is understanding why it matters beyond accounting, and how it actually affects your day-to-day cash decisions.

Build AP and cash flow projections your vendors and lenders will take seriously

Why accounts payable affects small-business cash flow

Every invoice you receive comes with a timing decision. You can pay early, pay on time, or stretch within your terms. That choice directly affects how much cash stays in your business. Many of the common cash flow problems small businesses face don’t come from a lack of revenue. They come from poor timing of inflows and outflows, and AP sits right at the center of that.

The Federal Reserve’s Small Business Credit Survey consistently ranks uneven cash flow among the top challenges small businesses report. The SBA’s financial management guide flags late payments as a recurring pressure point for small suppliers.

There are three ways I usually think about using AP on purpose.

- First, payment terms. If you can move a vendor from net 30 to net 45 or net 60, you extend your cash runway without changing your revenue. Most vendors will consider this if you’ve been paying reliably on time. It costs them nothing except a bookkeeping update and buys you real flexibility.

- Second, early-payment discounts. A 2/10 net 30 discount works out to roughly 36% annualized return on the cash you use to pay early. For most small businesses, that’s a better return than holding the cash, as long as your liquidity supports it.

- Third, timing. Large payments don’t need to be random. Aligning them with when cash actually comes in reduces pressure without changing your obligations. If most of your revenue lands in the first week of the month, schedule your big AP payments for the second week.

Say you carry an average accounts payable balance of $50,000. If you extend your payment timing by 10 days, that’s roughly $1,370 in additional working capital sitting in your business on any given day ($50,000 × 10 ÷ 365). You haven’t changed your operations, your revenue, or your obligations. The only thing that changed is when you paid.

This is where planning comes in. AP decisions belong inside your financial plan.

If you’re setting up a new accounting firm, our ready-to-submit accounting business plan template covers how to model payment timing into your cash flow. For bigger cash commitments like equipment or office buildouts, our guide on planning major purchases without hurting cash flow walks through the timing side.

How accounts payable shows up on your financial statements

Accounts payable show up across all three financial statements.

On the balance sheet, accounts payable appear under current liabilities. It represents what your business still owes. When your AP balance grows, your obligations grow too, even though your cash hasn’t moved yet. This gives you the clearest view of how much you still need to pay.

On the income statement, accounts payable doesn’t appear directly. The related expense shows up instead. The moment you record an invoice, the expense reduces your profit, even though the payment hasn’t happened. This is why profit can drop while your bank balance stays the same.

On the cash flow statement, the timing difference becomes visible. An increase in AP adds back to cash from operations, because you’ve recorded expenses without paying them yet, so the cash stays in the business.

When I review financials, I always look at AP alongside cash flow. Rising payables with stable cash can signal delayed payments. Falling payables with tight cash can signal that you’re paying too quickly. That’s the kind of distinction that changes how you understand the financial section of your business plan and where your cash is actually going.

How to forecast accounts payable

At a basic level, accounts payable is driven by two things:

- Your expenses

- Your payment terms

If your business incurs costs but doesn’t pay them immediately, a portion of those expenses will sit as payables. The longer your payment window, the larger that balance becomes.

I usually think of it this way. If your monthly expenses are consistent and your vendors give you 30-day terms, you’ll always be carrying about one month of expenses in accounts payable. If those terms stretch to 45 or 60 days, that balance grows without any change in actual spending.

A simple way to estimate this:

Projected AP = (Monthly expenses × Payment delay in days) ÷ 30

If your monthly expenses are $50,000 and you typically pay in 45 days, your projected AP would be around $75,000. That’s money you’ve committed to spend but haven’t paid yet.

Most founders project their expenses correctly, but assume cash leaves at the same time the expense hits the books. It doesn’t. That delay creates the gap between your income statement and your cash flow projections.

If you don’t have historical data, start with your agreed vendor terms. Most small businesses assume net 30, but in practice, payments often stretch to 35 or 40 days. Building in a small buffer keeps your forecast realistic rather than optimistic. Our guide on how to forecast without historical data walks through the full process for new businesses.

If you’re building a financial model, this is the piece that connects your expenses to your cash flow. If you already track AP in QuickBooks, Upmetrics integrates with QuickBooks for forecasting, so your payment timing flows straight into your projections. Without that connection, your projections might look accurate on paper but won’t reflect how money actually moves through your business.

Manage and track accounts payable in Upmetrics

If you’re building a business plan or financial forecast, your accounts payable assumptions shouldn’t sit separately from your numbers. They need to be connected to your expenses and cash flow; your projections won’t reflect reality.

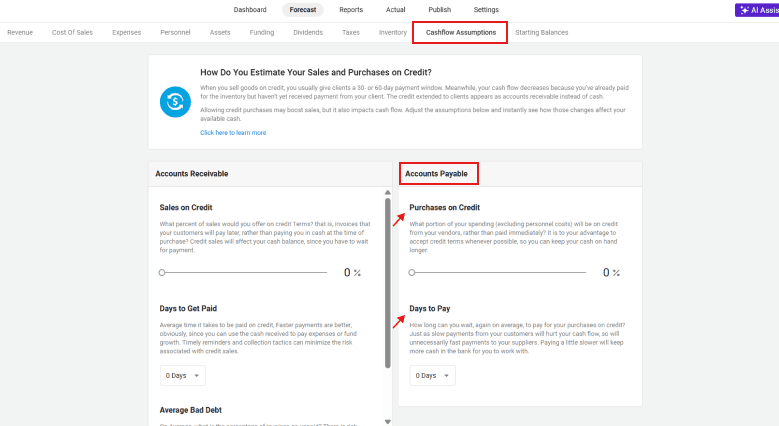

Upmetrics handles this through the Cashflow Assumptions tab inside the Forecast builder, where you can define how your payables behave alongside receivables. If you use Xero for your bookkeeping, you can connect Xero to your business plan and pull your actual AP data straight into the forecast.

Forecasting accounts payable

Under the Accounts Payable section, you typically define:

- Purchases on Credit: the portion of your expenses that won’t be paid immediately

- Days to Pay: the average number of days you take to pay vendors

These inputs control how much of your expenses remain unpaid at any point. If you adjust your payment timing, your cash flow updates automatically.

Tracking accounts payable

Once your assumptions are set, Upmetrics generates payable reports under the Reports section. These are available in monthly, quarterly, and yearly views, so you can see how your outstanding obligations build and clear over time.

Instead of tracking invoices manually, you get a structured view of what you owe and when it’s expected to be paid. That makes it easier to plan payments, avoid surprises, and keep your cash flow aligned with your actual obligations.

![]()

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.